Buying a home in 2026 looks very different from what it did just a few years ago. With shifting mortgage rates, rising home prices, and more inventory finally returning to the market, homebuyers need to stay informed and strategic.

This guide combines expert home-buying tips with the latest mortgage rate trends to help U.S. buyers make confident, smart decisions in today’s market.

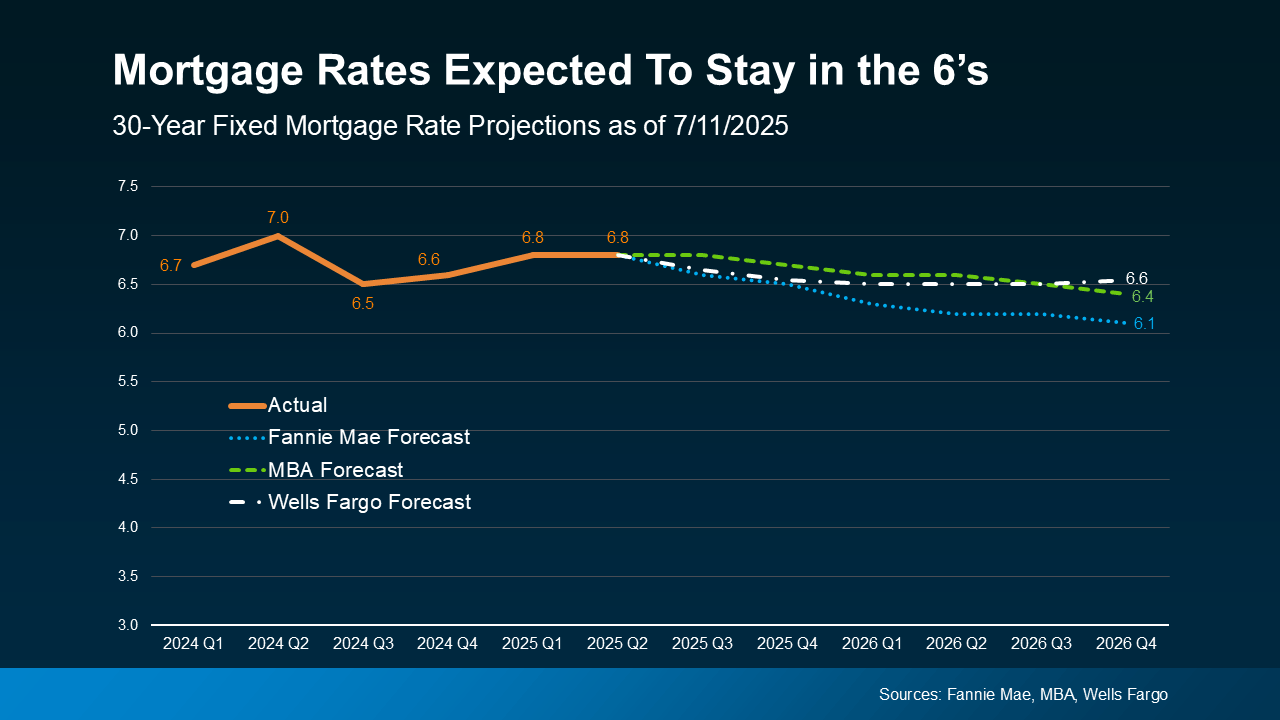

🔹 1. Mortgage Rate Overview (2026 Update)

Mortgage rates remain a major factor influencing buying power. While rates are still higher than pre-pandemic levels, they have become more stable.

Average U.S. Mortgage Rates (2026):

- 30-Year Fixed: 6.1% – 6.8%

- 15-Year Fixed: 5.2% – 5.7%

- FHA Loans: 5.6% – 6.3%

- VA Loans: 5.3% – 6.0%

- 5/1 ARM: 5.5% – 6.2%

Trend Insight:

Economists expect a gradual rate easing later in the year if inflation continues to cool.

🔹 2. What Today’s Rates Mean for Buyers

✔ Higher rates reduce how much home you can afford

A 1% rate increase can reduce buying power by up to $40,000–$60,000.

✔ Monthly payments remain elevated

Buyers must budget carefully and avoid stretching finances too thin.

✔ Locking early can protect you

Rate locks help buyers shield themselves from sudden increases.

✔ Refinancing may be an option later

If rates fall, you can refinance to lower payments.

🔹 3. Smart Home Buying Tips for 2026

Buying in 2026 requires a mix of preparation and strategy.

1️⃣ Get Pre-Approved Before You Start Shopping

A pre-approval:

- Shows your true price range

- Helps you compete with other buyers

- Allows you to lock in a rate early

Sellers take pre-approved buyers more seriously.

2️⃣ Improve Your Credit Score for Better Rates

Higher credit = lower payments.

Aim for:

- 620+ minimum

- 680+ for better pricing

- 740+ for premium rates

Pay down credit cards, avoid new accounts, and fix any errors.

3️⃣ Consider Homes Slightly Below Your Max Budget

With higher rates, buying below your limit gives you:

- Flexibility

- Safer monthly payments

- Room for emergencies

Never shop at your “maximum” number.

4️⃣ Don’t Skip the Home Inspection

Hidden issues can cost thousands.

Always inspect the:

- Roof

- HVAC

- Plumbing

- Foundation

- Electrical

If problems exist, you can negotiate a lower price.

5️⃣ Ask for Seller Concessions

In 2026, sellers are more open to negotiation.

You can request:

- Closing cost assistance

- Repairs

- Appliance credits

- Rate buydown contributions

A 2-1 buydown can lower your first-year payment significantly.

6️⃣ Explore Down Payment Assistance (DPA)

Many states offer:

- Grants

- Forgivable loans

- First-time buyer credits

DPA can help with:

- Down payment

- Closing costs

- Interest rate reduction

Programs are widely available in CA, TX, FL, OH, GA, NC, and NY.

7️⃣ Compare Lenders – Don’t Choose the First Quote

Rates vary significantly from lender to lender.

Compare:

- Interest rates

- APR

- Closing costs

- Points

- Fees

Just one comparison can save thousands.

🔹 4. How Mortgage Rates Affect Home Affordability

Example: $400,000 Loan – 30-Year Fixed

| Rate | Monthly Payment | Difference |

|---|---|---|

| 7.0% | $2,661 | – |

| 6.5% | $2,528 | Saves $133/mo |

| 6.0% | $2,398 | Saves $263/mo |

| 5.5% | $2,271 | Saves $390/mo |

Lower rates = significantly more affordable monthly payments.

🔹 5. Should You Buy Now or Wait?

Buy Now if:

✔ You find a home in your budget

✔ You need to move

✔ You want to build equity sooner

✔ You plan to refinance later

Wait if:

✔ You need time to save

✔ Your credit score needs improvement

✔ You expect lower rates later in the year

There is no universal answer – only what works best for your situation.

⭐ Conclusion

Buying a home in 2026 requires staying informed about mortgage rates and using smart strategies to maximize your buying power. With careful planning, strong lender comparison, and the right timing, you can successfully navigate today’s housing market and find a home that fits both your lifestyle and your budget.

Homeownership is a long-term investment – and understanding today’s rates helps you make the best financial decision.