Homeowners across the United States are sitting on record levels of equity – and in 2026, many are exploring refinancing options to lower their mortgage payments, consolidate high-interest debt, or fund major life expenses.

Whether you’re looking to tap into your home’s value or secure a better mortgage rate, understanding how home equity and refinancing work is essential to making smart financial choices.

This guide breaks down the latest home equity trends, the best refinance options, and how to decide which strategy works for your financial goals.

🔹 1. What Is Home Equity? Why It Matters in 2026

Home equity represents the portion of your home that you truly own.

Home Equity Formula:

Home Value – Mortgage Balance = Home Equity

Why equity is growing fast:

- Home prices have risen nationwide

- Mortgage balances shrink with every payment

- Demand for homes continues in many markets

In 2026, many U.S. homeowners will have $100,000 – $300,000+ in available equity, making this one of the best times to explore refinancing options.

🔹 2. Top Ways to Use Home Equity in 2026

Homeowners can use equity for almost anything, but the most common uses include:

✔ Debt consolidation

Paying off high-interest credit cards with a low-rate mortgage loan.

✔ Home improvements

Kitchens, bathrooms, roofing, windows, solar upgrades, etc.

✔ Emergency or medical expenses

Accessing immediate funds at a lower rate than personal loans.

✔ Education or tuition costs

✔ Investment opportunities

Rental properties, business starts, etc.

Using equity can be a smart financial move when managed responsibly.

🔹 3. Best Home Equity Options for Homeowners

There are three main ways to borrow against home equity:

✔ 1. Cash-Out Refinance

Replaces your current mortgage with a larger loan and gives you the difference in cash.

Pros:

- Lower fixed rate than credit cards

- One monthly payment

- Can remove PMI

Cons:

- Closing costs

- You restart your mortgage term

✔ 2. Home Equity Loan

A second mortgage with a fixed rate and fixed monthly payment.

Pros:

- Predictable payments

- Doesn’t change your primary mortgage

- Good for one-time expenses

Cons:

- Two mortgage payments

- Higher rates than cash-out refi (but still lower than credit cards)

✔ 3. HELOC (Home Equity Line of Credit)

A flexible line of credit you can borrow from as needed.

Pros:

- Only pay interest on what you use

- Ideal for ongoing projects

- Can be used repeatedly

Cons:

- Variable rates

- Payment amounts can change

🔹 4. Should You Consider Refinancing in 2026?

Refinancing isn’t only for lowering your rate – it can also help restructure debt or improve your monthly cash flow.

Refinancing makes sense if:

✔ Your mortgage rate is higher than today’s market rate

✔ Your credit score is higher than when you bought the home

✔ You want to cash out equity

✔ You want to switch from ARM to fixed

✔ You want to shorten your term (30 → 15 years)

✔ You want to remove PMI

Refinancing may NOT be a good idea if:

❌ You’re moving soon

❌ Your current rate is lower than new rates

❌ You can’t benefit more than the closing costs

🔹 5. 2026 Refinance Rate Trends

Mortgage rates are slowly stabilising, and many experts predict potential drops toward the end of the year.

Key 2026 refinance trends:

- More homeowners are using cash-out refinancing

- HELOC demand is increasing due to flexible borrowing

- Strong equity levels are boosting refi activity

- Many borrowers are waiting for rate dips

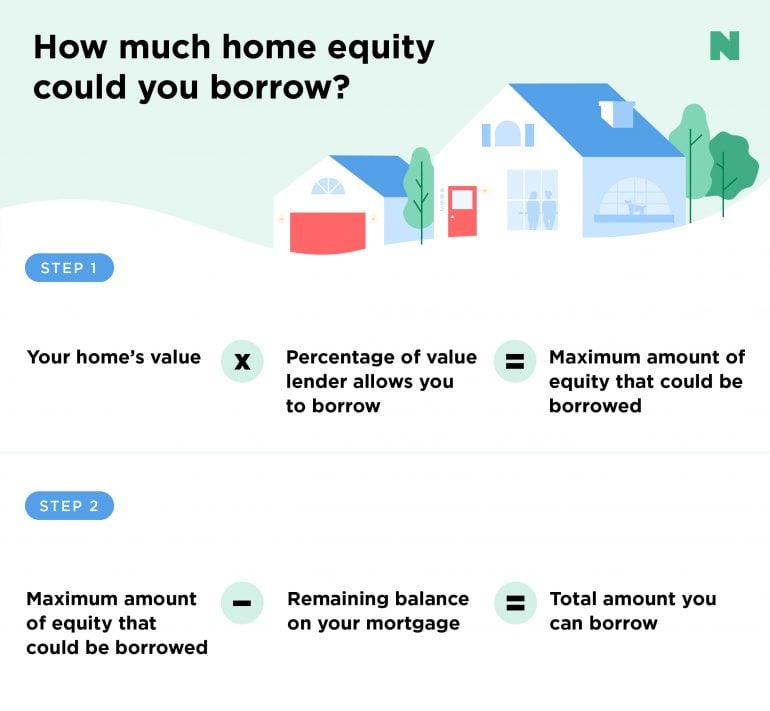

🔹 6. How Much Home Equity Can You Borrow?

Most lenders allow:

📌 Up to 80% – 85% CLTV (combined loan-to-value)

Example:

- Home value: $520,000

- Max allowed at 80% CLTV: $416,000

- Current loan: $265,000

Available equity to borrow: $151,000

🔹 7. Home Equity vs. Refinance: Which Should You Choose?

Choose a Home Equity Loan if:

✔ You want fixed, predictable payments

✔ You need a set amount of money

✔ You don’t want to change your main mortgage rate

Choose HELOC if:

✔ You want flexibility

✔ You have ongoing expenses

✔ You want access to funds over time

Choose Cash-Out Refinance if:

✔ You want the lowest possible rate

✔ You need a large amount of cash

✔ You want to combine your payments

✔ You want to remove PMI

🔹 8. Tips to Maximise the Benefits of Your Equity

✔ Improve your credit score before applying

Better credit = lower rates.

✔ Compare multiple lenders

Rates and closing costs vary widely.

✔ Only borrow what you can comfortably repay

Your home is the collateral.

✔ Check if interest may be tax-deductible

Applies only to home improvement usage.

✔ Understand your long-term goals

Are you improving your home, or reducing monthly debt?

⭐ Conclusion

Home equity and refinancing are powerful tools for U.S. homeowners in 2026. With rising property values and stabilising interest rates, now is a strategic time to evaluate whether tapping into your home’s equity can improve your financial future.

Whether you’re looking to lower monthly payments, consolidate debt, or access cash for major expenses, understanding your refinance options is the first step toward smarter homeownership.