Home equity has become one of the most valuable financial tools for American homeowners. With rising property values across the country and shifting mortgage rates in 2026, many households are exploring refinancing and equity-based loans to improve cash flow, consolidate debt, or fund major expenses.

This guide explains how home equity works, when refinancing makes sense, and how to choose the best option for your financial goals.

🔹 1. What Is Home Equity?

Home equity is the difference between:

Your home’s current market value – What you still owe on your mortgage

Example:

- Home value: $450,000

- Loan balance: $250,000

Your equity = $200,000

As home prices rise or as you pay down your loan, your equity grows – giving you financial leverage you can borrow against.

🔹 2. Ways Homeowners Can Access Home Equity in 2026

Homeowners have three main options:

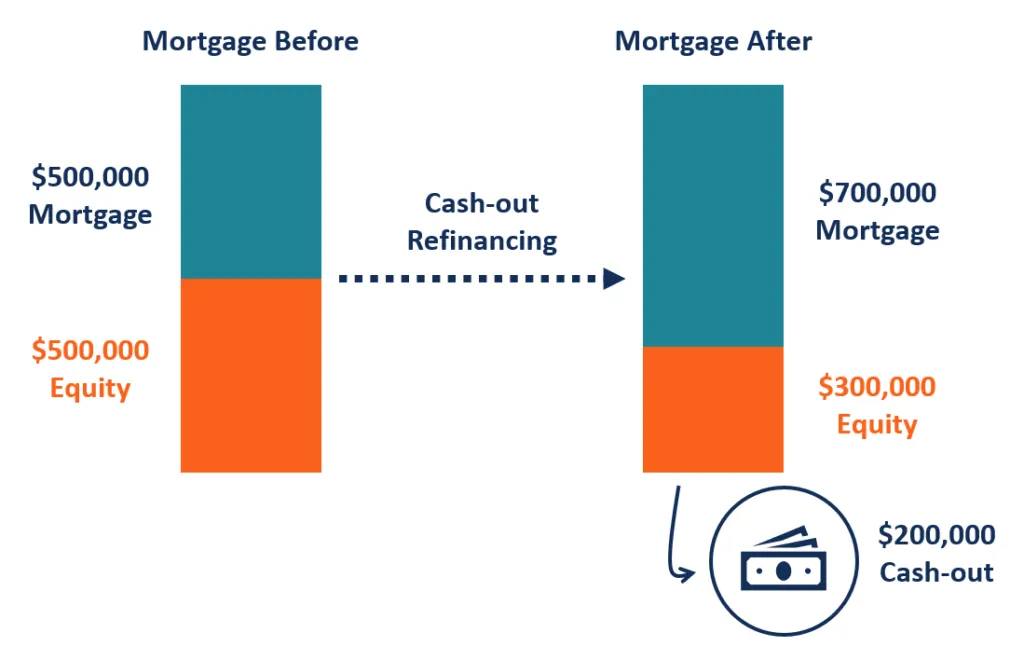

✔ 1. Cash-Out Refinance

You replace your current mortgage with a new, larger one – and take the difference in cash.

Best for:

- Paying off high-interest credit card debt

- Home improvements

- Major expenses (tuition, medical bills)

- Lowering your interest rate if current rates are favorable

✔ 2. Home Equity Loan (Second Mortgage)

You keep your original mortgage and take a second loan secured by your equity.

Best for:

- Homeowners who want fixed monthly payments

- Borrowers who don’t want to change their first mortgage rate

- Large projects with predictable costs

✔ 3. HELOC (Home Equity Line of Credit)

A revolving credit line you can borrow from as needed.

Best for:

- Ongoing home renovations

- Emergency funds

- Flexible borrowing needs

HELOCs often have variable rates, so payments may change over time.

🔹 3. When Does Refinancing Make Sense in 2026?

Refinancing can save money – but only in the right situations.

Refinance if:

✔ You can reduce your interest rate by 0.50% or more

✔ Your credit score has improved significantly

✔ You want to switch from an ARM to a fixed-rate loan

✔ You want to cash out equity at a favorable rate

✔ You want to remove PMI (private mortgage insurance)

Avoid refinancing if:

❌ You plan to sell the home soon

❌ New rates are worse than your current rate

❌ Closing costs would outweigh the savings

❌ Your credit score recently dropped

🔹 4. Benefits of Using Home Equity

✔ Lower interest than credit cards

Home equity loans typically have much lower rates than unsecured debt.

✔ Large borrowing capacity

You may access tens of thousands or even hundreds of thousands.

✔ Funds can be used for almost anything

- Home improvements

- College tuition

- Debt consolidation

- Big purchases

✔ Potential tax benefits

Interest may be tax-deductible if used for home improvements (consult a tax professional).

🔹 5. Risks You Should Consider

Accessing equity is powerful, but not without risks.

⚠ You could lose your home if you default

Equity loans are secured by your property.

⚠ Variable interest rates can increase payments

Especially with HELOCs.

⚠ Your total mortgage balance increases (cash-out refi)

⚠ Home values can decline

Equity is not guaranteed.

Always compare offers and evaluate long-term affordability.

🔹 6. How Much Equity Can You Borrow in 2026?

Most lenders allow:

- Up to 80% – 85% combined loan-to-value (CLTV)

Example:

Home value: $500,000

Max borrowable at 80% CLTV: $400,000

Current mortgage: $260,000

Available equity: $140,000

🔹 7. 2026 Market Outlook for Refinancing

With mortgage rates stabilizing and inflation gradually easing, many experts expect more refinance activity in the second half of 2026

Trends to watch:

- Potential lower rates

- More cash-out refinances

- Strong home equity totals due to rising home values

- Increased HELOC demand

If rates drop significantly, a major refi wave may return.

⭐ Conclusion

Home equity and refinancing offer powerful opportunities for U.S. homeowners to improve their financial stability, consolidate debt, or fund major expenses. With the right strategy, you can lower monthly payments, access cash, and position yourself for long-term financial success.

Understanding your options is the key to choosing the best solution – and 2026 is shaping up to be a strong year for homeowners evaluating refinance and equity strategies.