Mortgage rates continue to shape the U.S. housing market more than any other factor. As 2026 unfolds, homebuyers are watching rates closely while planning purchases, refinancing timelines, and affordability strategies. Whether you’re buying your first home or waiting for the right moment to lock in a rate, staying informed is essential.

This updated guide explains the latest mortgage rate movements, key market drivers, and what buyers can expect for the rest of 2026.

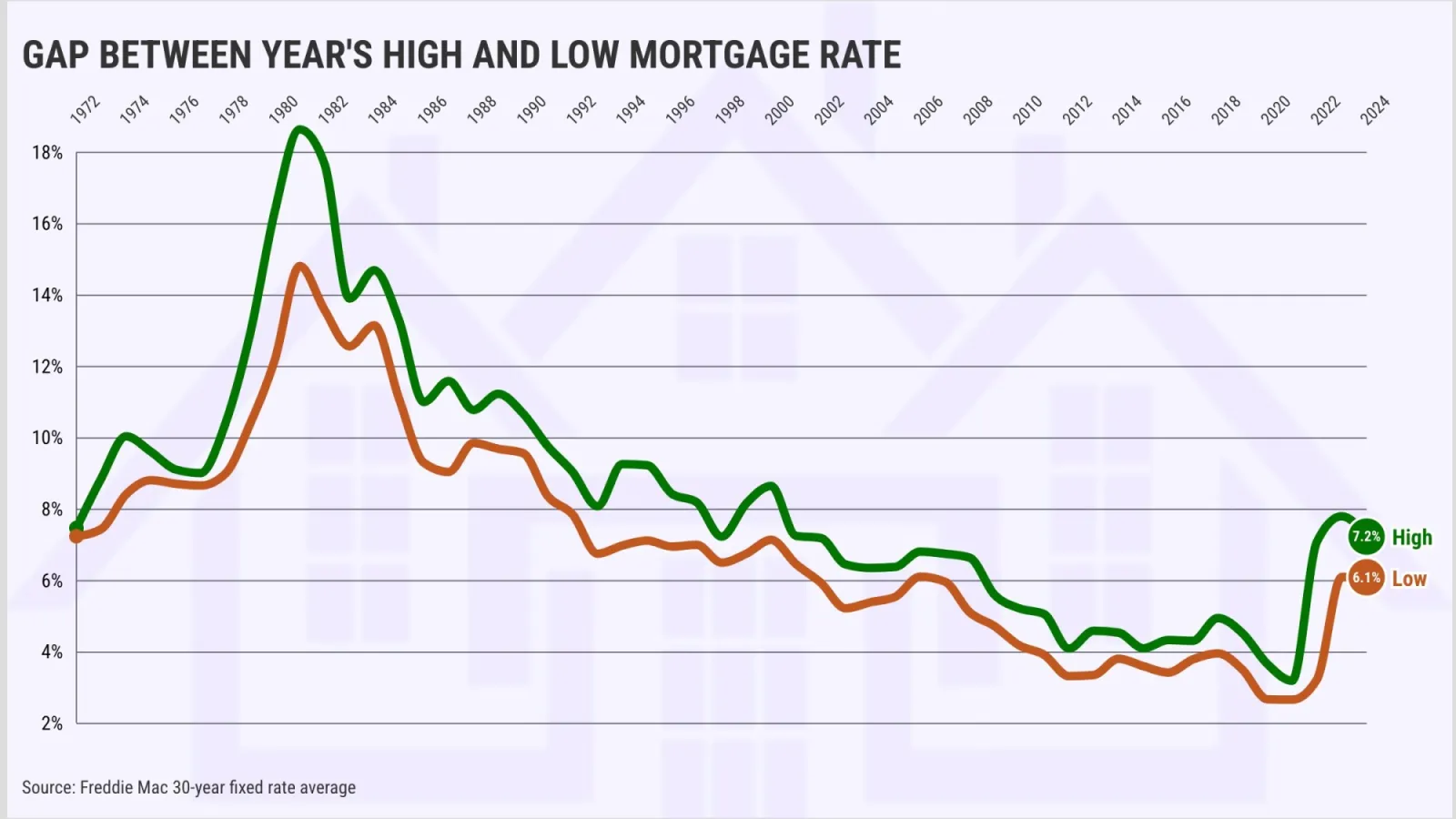

🔹 1. Current U.S. Mortgage Rates (2026 Snapshot)

Mortgage rates have stabilized compared to the extreme volatility seen from 2022–2024. While still elevated, the market is more predictable – and that’s good news for buyers.

Average Mortgage Rates (2026):

- 30-Year Fixed: 6.2% – 6.9%

- 15-Year Fixed: 5.1% – 5.7%

- FHA Loan: 5.5% – 6.3%

- VA Loan: 5.1% – 6.0%

- 5/1 ARM: 5.4% – 6.2%

Rates vary by:

- State

- Credit score

- Down payment

- Loan type

- Housing market demand

🔹 2. What’s Driving Mortgage Rates in 2026?

Mortgage rates respond to several nationwide economic factors:

✔ Federal Reserve Policy

While the Fed doesn’t set mortgage rates directly, its decisions strongly influence them.

If inflation declines, rate cuts become more likely.

✔ Inflation Trends

High inflation = higher mortgage rates

Falling inflation = potential future rate drops

✔ Bond Market Movements

Mortgage rates closely follow the 10-year Treasury yield.

When yields drop, mortgage rates often follow.

✔ Housing Market Activity

Strong buyer demand can push rates higher; slower demand can stabilize them.

🔹 3. Will Mortgage Rates Drop in 2026?

Many analysts believe that if inflation cools and the Fed shifts toward rate cuts, mortgage rates may decline gradually throughout late 2026.

Possible Outcomes:

- Small rate reductions (not huge drops)

- Increased affordability later in the year

- Stronger refinance activity

However, rates will likely not return to the historically low levels of 2020–2021.

🔹 4. How Mortgage Rates Impact Your Buying Power

Even tiny rate changes can dramatically shift affordability.

$450,000 Loan – 30-Year Fixed

| Rate | Monthly Payment | Difference |

|---|---|---|

| 7.0% | $2,993 | – |

| 6.5% | $2,844 | Saves $149/mo |

| 6.0% | $2,697 | Saves $296/mo |

| 5.5% | $2,552 | Saves $441/mo |

A drop from 7.0% → 6.0% can save nearly $3,500 per year.

🔹 5. Should You Lock Your Mortgage Rate Now?

Rate locks protect you from future increases – but timing matters.

Consider locking if:

✔ You found the right home

✔ Rates are trending upward

✔ You’re closing soon

✔ You want predictable payments

Consider floating if:

✔ Rates are slowly declining

✔ You’re weeks or months away from closing

✔ Economic news signals future cuts

For many buyers, locking is the safer choice in uncertain markets.

🔹 6. Tips to Get a Lower Rate in 2026

✔ Improve your credit score

Aim for 680+, ideally 740+ for the best pricing.

✔ Increase your down payment

Bigger down payment = lower risk = better rate.

✔ Compare at least 3–5 lenders

Rates differ more than most buyers realize.

✔ Choose the right loan type

VA, FHA, and USDA loans often offer lower-than-market rates.

✔ Avoid major credit changes

No new accounts or large purchases before closing.

🔹 7. Refinancing Outlook for 2026

Refinancing slowed in recent years due to higher rates, but homeowners are planning for potential drops.

Refinance activity may increase if:

✔ Rates fall below current averages

✔ Homeowners have strong equity

✔ Borrowers want to consolidate debt

Cash-out refinances and HELOCs remain popular due to high home values.

⭐ Conclusion

Mortgage rates continue to shape the 2026 housing market, influencing everything from buying power to home affordability. While current rates remain elevated, stability has returned – and gradual improvements may come as inflation cools.

Staying informed gives buyers a competitive advantage. Whether you’re considering a purchase now or watching for a better rate later, understanding today’s trends is the first step toward confident homeownership