The U.S. mortgage market in 2026 continues to shift rapidly as interest rates react to inflation, Federal Reserve policy, and housing demand. Whether you’re buying your first home, refinancing, or watching the market to time your move, staying updated on mortgage rate trends is essential.

This guide explains the latest mortgage rate movements, what’s driving them, and how today’s rates impact affordability for American homebuyers.

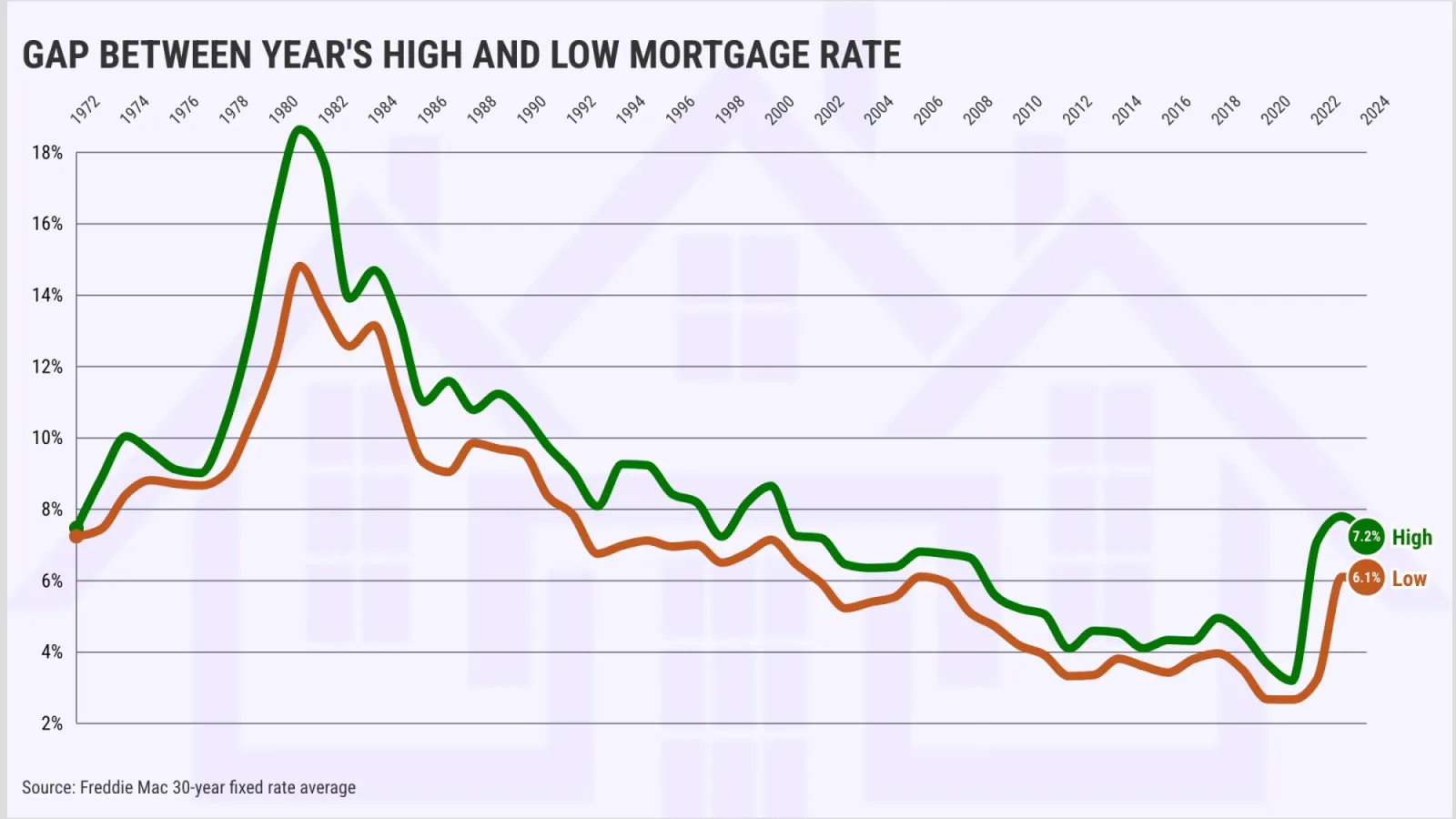

🔹 1. Current Mortgage Rate Overview (2026)

Mortgage rates in 2026 remain higher than pre-pandemic levels, but have begun showing signs of stabilization as inflation gradually cools.

Average U.S. Mortgage Rates (Early 2026):

- 30-Year Fixed: 6.2% – 6.9%

- 15-Year Fixed: 5.3% – 5.8%

- FHA Loans: 5.8% – 6.4%

- VA Loans: 5.5% – 6.1%

- 5/1 ARM: 5.7% – 6.3%

Rates vary based on:

- Credit score

- Down payment

- Loan type

- Location

- Lender

- Overall market conditions

Even a 0.25% change in rates can significantly affect monthly payments.

🔹 2. What’s Driving Mortgage Rates in 2026?

Mortgage rates don’t move at random – they reflect larger economic forces.

✔ Federal Reserve Policy

When the Fed raises or cuts rates, mortgage rates usually follow.

✔ Inflation

High inflation causes higher rates. Lower inflation helps reduce rates.

✔ Housing Market Demand

- High buyer demand = higher rates

- Slow markets = more competitive rates

✔ Bond Market Activity

Mortgage rates follow the 10-year Treasury yield, a key economic indicator.

These factors create the dynamic rate environment homebuyers see today.

🔹 3. What Rising or Falling Rates Mean for Homebuyers

If rates rise:

- Monthly payments increase

- Buying power drops

- Home affordability decreases

- Refinancing becomes less attractive

If rates fall:

- Buyers qualify for larger loan amounts

- Monthly payments decrease

- Refinancing opportunities increase

- More homeowners may enter the market

🔹 4. Mortgage Payment Example (To Show Real Impact)

Loan Amount: $400,000

Term: 30-Year Fixed

| Interest Rate | Monthly Payment | Difference |

|---|---|---|

| 7.0% | $2,661 | – |

| 6.5% | $2,528 | Saves $133/mo |

| 6.0% | $2,398 | Saves $263/mo |

| 5.5% | $2,271 | Saves $390/mo |

A lower rate dramatically improves affordability.

🔹 5. Should You Lock Your Rate in 2026?

A mortgage rate lock protects you from future increases.

Consider locking if:

- You’re closing soon

- Rates are trending upward

- Your loan approval is complete

- You want predictable payments

Consider floating if:

- Rates are trending downward

- You have months before closing

- Inflation is falling

- The Fed signals future cuts

A mortgage expert can help analyze timing.

🔹 6. Tips to Get a Lower Mortgage Rate in 2026

✔ Improve your credit score

Aim for 700+, ideally 740+.

✔ Increase your down payment

20%+ often unlocks the best rates.

✔ Compare multiple lenders

Never take the first offer – lenders vary widely.

✔ Consider loan types

VA, FHA, and USDA loans often offer below-market rates.

✔ Avoid major purchases

Keep your debt-to-income (DTI) ratio low during approval.

🔹 7. Should You Refinance in 2026?

Refinancing makes sense if:

- You can lower your rate by 0.50% or more

- You want to shorten your loan term

- You want to remove PMI

- Your credit score improved significantly

Refinancing can save thousands over the life of the loan.

⭐ Conclusion

Mortgage rates in 2026 remain unpredictable, but with the right timing and strategy, homebuyers can still secure affordable financing. Staying informed about rate trends is essential – especially in a competitive housing market.

Whether you’re buying, refinancing, or planning for the future, monitoring mortgage updates helps you make confident, smart financial decisions.